How to market a Semiconductor company in China

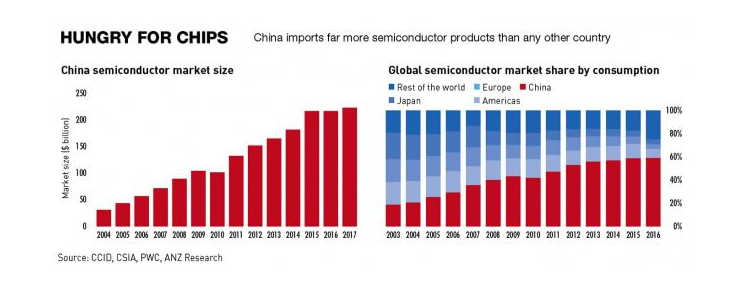

China’s Semiconductor Industry: 60% of the global semiconductor consumption. It is a huge market in China.

SILICON | Would china be able to make chips?

Cost-Effective Agency

KPI and Results focused. We are the most visible Marketing Agency for China. Not because of huge spending but because of our SMART Strategies. Let us help you with: E-Commerce, Search Engine Optimization, Advertising, Weibo, WeChat, WeChat Store & PR.

source

At the danger of sounding excessively negative, let us talk about China’s semiconductor fab/foundry circumstance. Fabs are one of the central reasons, it is challenging to envision China getting autonomous from coordinated circuit (IC) imports: no place in China can make bleeding-edge chips. The semiconductor autonomy “Enormous Reserve” has organized the region. So let us see this critical piece of the IC business: genuinely making the chips. The growth of China’s semiconductor industry is huge

Chinese semiconductor Market

- The semiconductor market in China is the largest in the world.

- China consumes more than 50 percent of all semiconductors, both for internal use and eventual export.

- The local Chinese factories are still only capable of meeting approximately 30% of their own demand.

If you want to develop your Semiconductor in China

Read this

https://seoagencychina.com/lead-generation-7-keys-success-china/

What is a fab?

See on CNBC

A fab or foundry is a processing plant where semiconductors are manufactured. To produce forefront chips, fabs need capital hardware from everywhere throughout the world, the most exceptional of which are from Europe, the US, and Japan. What goes on inside fabs is likened to speculative chemistry. It could be said, at any rate, while talking about silicon chips, they are utilizing gear from organizations, for example, ASML and LAM, to transform sand into a disk. This is not an industry you get into spontaneously.

One ASML photolithography machine—a solitary piece of the generation line—costs about $100 million. Incorporated gadget producers like Intel work their fabs; however, today, we are taking a gander at “unadulterated play.” Unadulterated play fabs do not use configuration chips, albeit some work intimately with configuration administration accomplices. They, by and large, especially make chips for “fabless” IC organizations like HiSilicon or Qualcomm, getting structures as GDSII-type records.

How fab are China’s fabs?

The creatively named “Taiwan Semiconductor Assembling Partnership” (TSMC) commands the worldwide unadulterated play fab market with a near half piece of the overall industry. Samsung is a far off second at 18%. Third spot Worldwide Foundries from the US has just around 9% piece of the pie. There are two principal Chinese organizations in this industry: the “Semiconductor Assembling Industry Enterprise” (SMIC)— I think they were attempting to beat TSMC in the creative mind office—and Hua Hong.

These two have 5% and 1.5% worldwide pieces of the overall industry separately, with the majority of their deals inside China. While these two fabs are comprehensively serious in anything 28 nanometers (nm) or more, anything underneath is a battle, and the littlest procedures are the place the top-of-the-line chips are. Chinese fabs are behind, and it will be difficult for them to make up for lost time for a couple of reasons: access to. the most recent hardware, an absence of ability, and being late to the game.

Gear

It requires some investment for driving gear organizations to fabricate the most recent hardware. Organizations like ASML and LAM Exploration typically put their greatest clients first in the line. TSMC and afterward, Samsung will consistently be the preferred choice.

Further, gear creators can only with significant effort grow generation ability to get Chinese fabs quicker access to hardware like extreme ultraviolet photolithography (EUVL). The skills expected to make them are rare.

Geopolitics additionally impedes conveying the most recent gear on schedule—or more regrettable. A memory producer called Fujian Jinhua was cut off from this gear in late 2018 by a US trade boycott. With no option in contrast to the US and US-connected European providers, the organization needed to drop plans for a $6 billion plant, and it shows up is still not creating any chips.

Ability

The best ability typically goes to the best organizations. On the off chance that you are new alumni taking a gander at the business, you will need to go to TSMC or Samsung. Else, you may even pick an alternate industry. It is reasonably narr; however, every SMIC engineer (outside of the board) I have ever spoken with has whined of low wages and outrageous working hours—think 996, and in some cases far more atrocious. The night shifts are terrible. Presently the extraordinary working hours might be comparable at any semblance of TSMC; however the pay the circumstance is not.

To fill the ability hole, SMIC and others have been focusing on Taiwanese, South Korean, and Japanese architects with enormous pay rates and different advantages. A ton of Huge. Reserve cash has gone into such ability enlistment, which has helped win a few volunteers—yet could likewise cause considerably more disappointment among neighborhood engineers who are not getting paid as much as their outside companions. Until this point, the additional ability has not helped Chinese fabs get up to speed. Different obstacles are excessively extraordinary.

Timing

Chinese fabs were late to the game, have consistently been behind in fact, and, as referenced above, remain at the rear of the line with regards to acquiring gear. It does not work in each part, however here it indeed has been the first-mover advantage. SMIC came into the business 13 years behind TSMC, and after 19 years, it is still behind in fact and a long way behind financially. For instance, no Chinese fab had the option to make FinFET structures until this year.

Without going into subtleties, FinFET is the current best quality procedure, which can fit more transistors into a specific region utilizing a 3D structure. TSMC has been creating FinFET since the mid-2010s. After a few deferrals, some of which was because of US pressure on ASML, SMIC at long last declared that a 14nm FinFET generation line was ready for action two or three months back, merely beginning low volume runs, and claims to increase to large scale manufacturing right now. In the meantime, TSMC and Samsung are full-grown at 7nm, will have 5nm one year from now, and have started the development of a 3nm fab.

Possibilities?

China’s Semiconductor Enormous Reserve put resources into unadulterated play fabs and memory fabs with minimal recognizable outcome in these two zones up to this point, at any rate economically. In any case, watch this space. Enormous Reserve Imprint II, which raised RMB 200 billion (about $28 billion) in July, will probably keep on putting intensely in these regions. Yet, there is just so much tossing cash at issue can do. Industry lord producers like ASML are partly possessed by TSMC and Intel, making it hard for Chinese fabs to stretch out beyond the line for cutting edge gear, and given the affectability of the innovation, Chinese venture or obtaining appears to be far-fetched.

The primary way out of this bind is for Enormous Reserve Imprint II really to put its cash into making Chinese capital gear players. It appears as though this is a center, particularly plasma drawing gear. I envision terrain plasma drawing gear creator. Naura will get a portion of this cash to push past its current 14nm point of confinement. Yet, there is still no indication of a robust Chinese player in very good quality photolithography. Without one, Chinese fabs will, in any case, depend on remote innovation. We, as a whole, perceived how Fujian Jinhua faired after remote hardware providers all left.

While different nations are also reliant, China’s IC supply is in danger because of geopolitical reasons, and even with all the cash on the planet, it would not have its substitution gear at any point soon.