E-Commerce in China is Booming (data 2022)

E-commerce in China is booming in 2022, you will find in this article all data 2022 available on the internet. The Chinese e-commerce market is undoubtedly one of the most profitable and fastest-growing cyber industries in the world. This makes some rational international brands understand how to intelligently approach this extraordinary electronic retail market, which is an interesting proposition. To understand the future of e-commerce, we must move Eastward rather than Westward.

Trends in China

We expect more brands to engage with platforms such as Taobao Streaming, and to collaborate with apps such as Kuaishou in order to increase their online engagement.

Cost-Effective Agency

KPI and Results focused. We are the most visible Marketing Agency for China. Not because of huge spending but because of our SMART Strategies. Let us help you with: E-Commerce, Search Engine Optimization, Advertising, Weibo, WeChat, WeChat Store & PR.

Online shopping is a convenient way to shop for Chinese Netizens.

This trend will continue. Shopping via mobile in a mobile-first nation like China with 1.6 million mobile phone subscriptions can offer consumers greater convenience and accessibility. Pinduoduo’s success in rural and small-town areas is a testament to online shopping. Pinduoduo has actually harnessed the power and potential of the forgotten consumer to become the third-largest e-commerce player in China.

The Chinese economy rebounded from the pandemic effects. Alibaba reported a 30% increase in quarterly revenue as the demand for online commerce remained high. Alibaba (**, which reported a revenue of 155.1 billion yuan (USD 23.4 million) for the 3 rd quarter of 2020, was a success.

Alibaba is the Leader with Tmall & Taobao

Alibaba’s shares experienced a 60% increase in trading volume compared to March when the pandemic hit. They also managed to reach a record high in October 2020. Due to the increased demand from the retail and finance sectors, sales of their Cloud-based services grew by 60%. Alibaba has reached a significant milestone by making this the first profitable sector since its inception.

JD the challenger

jd.com is the largest player in China’s eCommerce Market. In 2021, the store generated total revenue of US$95.5 million. It is followed closely by Suning.com, which has a revenue of US$22.8 million, and Vip.com which has a revenue of US$14.9 trillion. The top three online stores in China account for 10% of China’s total revenue.

Rankings are determined based on the number of stores that have generated revenue in China. These stores can have a national focus, selling only in their home country, or they may be global. This evaluation only considered revenue generated in China.

A new one Aimer

aimer.com.cn is one of the most popular stores in China. In 2021, the store had sales of approximately US$49.2 million. The store’s revenue growth was 274% over the previous year.

We are an e-Commerce Agency specialized in China

What happened to e-commerce in China during the lockdown in 2022?

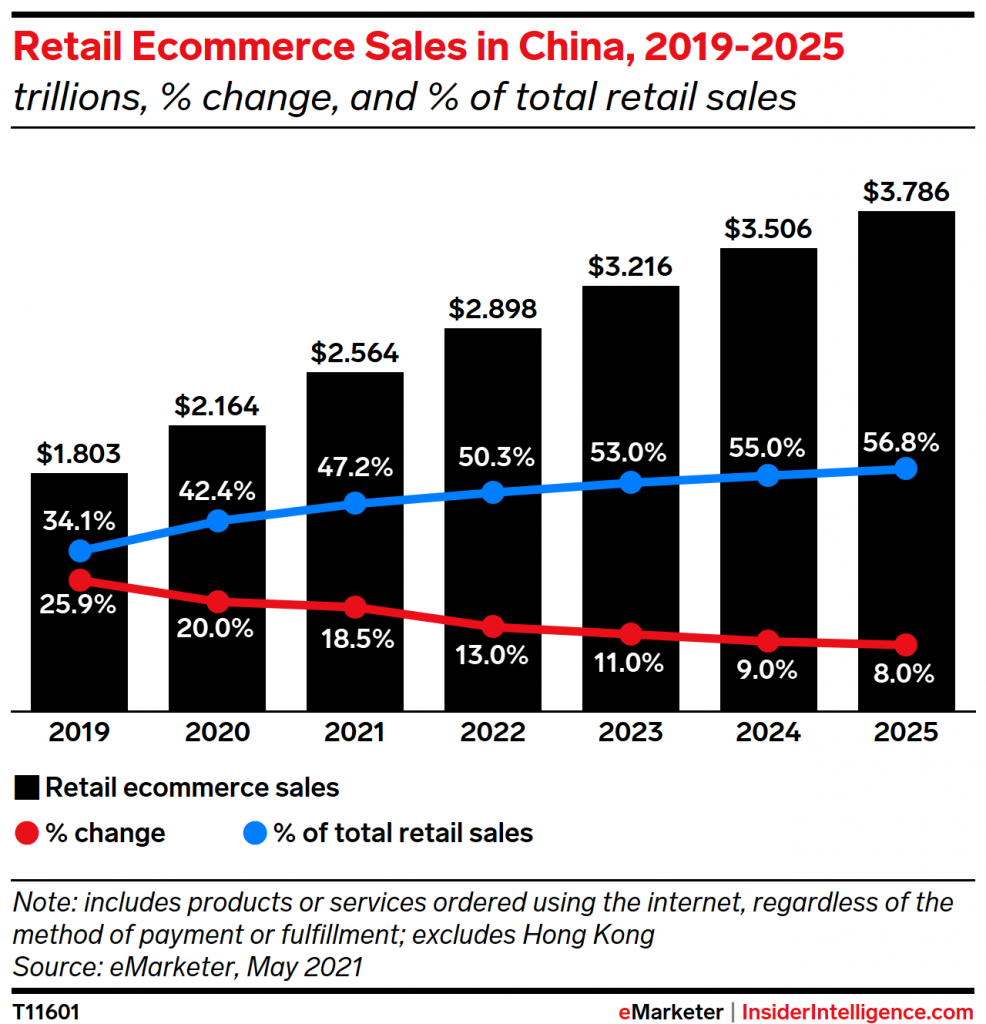

China’s eCommerce industry remained steady in 2022, but it did not explode as fast as we thought. Last year’s growth was 20.0%, which is 7.5 percentage points lower than what we expected. This resulted in a total of $2.164 trillion. We expect 18.5% growth this year. This is lower than China’s latest figures, but still the eighth fastest in the world. China will continue to dominate eCommerce worldwide (52.1%).

What are the prospects for China’s biggest eCommerce players in China?

Alibaba is still the largest eCommerce company in the world, but it had a disappointing 2020. It saw its share of China’s e-commerce market fall below 50% for the very first time. Pinduoduo (PDD), and JD.com have been growing faster. PDD will have a 13.2% market share in 2021, and JD.com will have a 16.9%. These three “Big Three” will control 77.2% this year.

Livestreaming eCommerce

If China’s live streamers of eCommerce were their country, they would be third in terms of retail eCommerce sales this year at $299.66 billion. Livestreaming eCommerce grew 160.0% last fiscal year, and it will continue to grow by 85.0% in the coming years.

What’s next in China’s social commerce?

China’s social commerce figures, which are $351.65 billion, are already 10x higher than those in the US. The new story is live streaming, which will increase by 95.5% and account for over 50% of social commerce by the next.

China’s retail eCommerce sales increased by 20% last fiscal year, which was less than the 27.5% growth we had previously forecast. We expect a slowdown in growth this year to 18.5%

GlobalData estimates that the Chinese e-commerce market will reach $3 trillion (19.6 Trillion RMB) by 2024. This is up from $2.1 trillion (13.8 Trillion RMB) in 2021. The CAGR for the next four years is 12.4 percent, according to GlobalData.

In 2022, E-commerce sales will grow by 17.2% in China due to the COVID-19 pandemic. While overall consumer spending fell by 3.9 percent in 2020, online sales increased by 14.8 percent in the same period.

The luxury sector will see a rapid increase in consumer spending due to the economic recovery. There are many policies in place to increase consumption. However, only the wealthy can afford ” revenge spending.”

As new players enter the online space, eCommerce sales will rise. E-commerce giants are continually trying to increase their conversion rates by using cutting-edge technologies.

Livestreaming and virtual reality (VR), as well as augmented reality (AR), features have already been shown to improve user interactions and experiences. Gamification elements such as those used by Tencent and Alibaba engage customers longer and increase buyer motivation.

15. ByteDance Inc., Douyin Flagship Store

Revenue: US$35 billion, 2020 source yahoo

Douyin launched its flagship store in March 2021, and brands can launch their own stores on the platform. Douyin was originally created to help consumers find new products and popular products. Although companies could send their followers vouchers and link to other e-commerce platforms, the real value of flagship stores is marketing. It is ranked 15th on our list of China’s largest e-commerce businesses.

These stores can help brands increase conversion rates. Users can not only create campaign banners and send them out, but they can also save information offline. More than 220 brands, including Winona and Peacebird from China, have launched their flagship stores since the launch. Douyin hopes to achieve 1 trillion Yuan in revenue by 2021, and compete with the top e-commerce players like Alibaba (NYSE: BABA), and JD.com.

14. Yihaodan, owned by JD.com Inc.

Revenue: US$1.8 billion, 2020

YihaodianJD was founded in 2008. It is an online shopping platform for grocery shopping. It uses a business-to-consumer (B2C) and connects consumers with farmers/distributors directly. Yihaodian (NASDAQ: JD), which operates “virtual shops”, has unique images of grocery items on public surfaces. People can scan the codes to add groceries to their shopping cart. It is ranked 14th on our list of China’s largest e-commerce firms.

In 2011, Walmart (NYSE: WMT), bought a 51% share in Yihaodan (NASDAQ; JD), but they acquired 100% ownership by 2015. Walmart (NYSE/WMT) and JD.com. (NASDAQ/JD) reached a $1.5 billion deal in 2016. In this deal, Walmart (NYSE/WMT) sold all its shares in Yihaodan for a 5% share in JD.com.

13. Autohome Inc.

Revenue: US$1.33 billion, 2020

Autohome, Inc. (NYSE: ATHM), a Beijing-based holding company, creates and maintains automobile websites and mobile apps. It is China’s largest e-commerce platform, selling new and used cars. It is ranked 13th on our list of China’s largest e-commerce businesses.

Autohome (NYSE ATHM), allows sellers to display their products via dealer subscriptions and advertising services. This allows sellers to extend the reach of their showrooms to millions more internet users. Autohome (NYSE ATHM), offers services such as used car transactions, auto insurance, auto financing, and aftermarket services.

12. E-commerce China Dangdang Inc. (DangDang)

Revenue: US$1.37 billion, 2020

Dangdang, a Chinese eCommerce company, was founded in 1999. It is headquartered in Beijing and its main competitors include Amazon (NASDAQ: AMZN) as well as JD.com (NASDAQ: JD). In 2010, the competition started a price war, with both Amazon (NASDAQ: AMZN) and JD.com (NASDAQ: JD) dropping prices on a wide variety of products, including books. It is ranked 12th on our list of China’s largest e-commerce firms.

Dangdang offers a wide range of products including household merchandise, digital, cosmetics, and home appliances as well as books, audio, clothing, and baby and maternal care products. DangDang has more than 10 million registered customers each year and over 100,000 people buy products from Dangdang every day.

The company competes with major players such as Alibaba (NYSE: BABA), Amazon.com, Inc., Walmart (NYSE: WMT), JD.com, and JD.com.

11. Xiaohongshu ( Little Red Book)

Revenue: US$1.49 billion, 2020

Xiaohongshu (also known as RED) is an eCommerce platform that has over 300 million users. It also boasts over 85 million active monthly users. It also runs RED Mall which sells international products for Chinese users. Users can also share their product reviews, travel stories, and lifestyle stories through short videos and photographs. It is ranked 11th on our list of China’s largest e-commerce firms.

Xiaohongshu started out as a platform where users could share product reviews. It has been focusing on its own e-commerce platform, where Chinese consumers can place orders from overseas, even though it was originally founded to allow users to share reviews of products.

Xiaohongshu was one of the largest community e-commerce platforms, with revenue of CNY=10 billion in 2017. They also launched REDelivery, an international delivery service. They also hosted a shopping festival in 2017 to celebrate their fourth year anniversary. It brought in sales revenue of over CNY= 100,000,000 in 2 hours.

10. Momo Inc.

Revenue: US$2.30 billion, 2020

Momo Inc. (NASDAQ: MOMO), Beijing-based social networking and entertainment platform is located in Beijing. Momo (NASDAQ, MOMO) makes revenue from mobile games, stickers, and paid emoticons, as well as paid membership subscriptions and marketing services. The platform is used by 85 million people to make connections based on location and their interests. Users can search for people, groups, and message boards, as well as find events and people based on their location. You can also create short videos and live streams via Momo’s (NASDAQ: MOMO) platform.

9. Jumei

Revenue: The figure for 2020 is unavailable

Jumei International (NYSE: JMEI), is a Beijing-based company that was established in 2010. China’s largest online seller of beauty products is the one with the highest sales volume. Jumei (NYSE: JMEI), sells luxury and branded cosmetics, skincare, and fragrances for babies, children, maternity, and other products. They use three strategies: curated, online shopping malls, and flash sales. Jumei Global (NYSE: JMEI), allows Chinese consumers easy access to overseas products and makes it simple and straightforward to make payments. It also has its own private label, and it sells products under that. It is ranked 9th on our list of China’s largest e-commerce firms.

The company competes with major players such as Alibaba (NYSE: BABA), Amazon.com, Inc., Walmart (NYSE: WMT), JD.com, and JD.com.

8. Pinduoduo Inc.

Revenue: US$4.07 billion, 2020

Pinduoduo Inc., PDD is China’s largest e-commerce platform for agriculture. It connects consumers and farmers directly. In 2019, approximately 600,000 farmers sold their farm produce through Pinduoduo. Pinduoduo has ambitious plans to increase its sales to $145 Billion per year by 2025.

It has introduced new trends to the market, such as social commerce and consumer-to-manufacturer (C2M), that have revolutionized e-commerce in China.

Pinduoduo had 731.3 million active customers (over the last year), and 643.4 million of them used the site monthly in 2020.

Duo Duo Maicai was launched in August 2020. This grocery service allows consumers to place orders online and pick them up the next day. It was created to provide a better way for consumers to purchase groceries during the pandemic.

7. 58.com Inc

Revenue: US$11.29 billion, 2020

58.com Inc. (NYSE: WUBA), was established in 2005 and is based out of Beijing. It is China’s largest online marketplace for classifieds and ads. This allows local sellers and buyers to exchange information and do business. The 58.com (NYSE: WUBA), the website offers a variety of listings from around 380 cities. These listings include real estate, employment, used goods and pets, tickets, yellow pages, and other local services. According to the firm’s data, the most popular category on 58.com (NYSE: WUBA) is job listings. They account for a significant portion of total revenue and grow the fastest. It is ranked 7th on our list of China’s largest e-commerce companies.

The company competes with major players such as Alibaba (NYSE: BABA), Amazon.com, Inc., Walmart (NYSE: WMT), JD.com, and JD.com.

6. NetEase, Inc. (Kaola)

Revenue: US$11.29 billion, 2020

NetEase was established in 1997 and is based out of Beijing. It provides IT solutions and services. These include advertising, gaming, and e-commerce. NetEase offers Chinese consumers a variety of e-commerce solutions on mobile and desktop. They also offer a platform for sellers and offer a range of products, including e-readers and matchmaking services. It is ranked 6th on our list of China’s largest e-commerce firms.

Kaola.com was launched by NetEase in 2015. It is similar to Amazon.com’s operations and has over 15 million users. Yanxuan is an international and private-label e-commerce company that NetEase (NASDAQ): NTES also operates.

The company competes with major players such as Alibaba (NYSE: BABA), Amazon.com, Inc., Walmart (NYSE: WMT), JD.com, and JD.com.

China’s e-commerce market

Statistics show everything. According to the National Bureau of Statistics of China, online retail sales in 2016 reached 5.16 trillion yuan ($ 752 billion), an increase of 26.2% over 2015, more than double the overall retail sales growth rate.

The report promises that China’s e-commerce sector will be ahead of the United States and four times more in the east than the United States.

Now is the time to enter this market. First, brands must understand best practices and trends that are shaping how you tailor their approach – capturing your pie.

E-commerce is not a “first-world phenomenon”

The growth of China’s e-commerce is incredibly driven by tier-3 and tier-4 cities, which surpassed tier-1 and tier-2 cities for the first time. The emerging trend to watch for is that the rural markets in the rest of emerging Asia will also experience significant e-commerce growth.

China’s GDP grew 7% over the same period last year, resulting in rising levels of wealth in third- and fourth-tier cities. In addition, these cities do not have the physical infrastructure of high street stores, so they rely more on electronic retail.

Alibaba, China’s e-commerce giant, also thanks to them for their nationwide investment in delivering infrastructure to increase access to rural areas and smaller urban areas.

China is a leading digital innovator

China now sets an innovative benchmark for this industry. China’s mobile digital payment system through WeChat and Alipay is just the tip of the iceberg. The convenience and security of electronic payments (connected to mobile banking in consumer banking) are often thought to be a key reason for the rise in e-retail spending. It is suitable for an instant, the impulsive purchase is just a screen credit card.

These mobile payment systems are accepted online and offline and are highly integrated into the lives of consumers making them the preferred payment method. Almost 500 million businesses in China use Alipay, and consumers now use it overseas even while traveling.

Alipay recently launched the “face-to-face payment”, so you can self-certified payment methods, which is the perfect solution for Asian countries. The ease of development and speed of purchase is where the rise of modern China is.

As consumers can digitally browse through virtual reality simulations, virtual reality shopping also erupts. Alibaba shows a demonstration of a BUY + virtual store that allows shoppers to ship themselves to New York City and actually walk the walkways of the famous Macy’s department store to buy selected items.

The rise of “social business”: WeChat, Little Red Book, Weibo

We already know that about 50% of e-commerce is driven by social media in many parts of Asia. Trends are the ability to buy directly from social platforms.

Chinese social media plays an important role in daily life. Tencent’s WeChat is integrating stores into their apps. This sets the tone for a new era of social-networking shopping experience on the social network.

It is logical that shopping and buying are encouraged by the experiences that can be shared. WeChat allows instant payments via the “wallet” feature while interacting with the official accounts through groups, IMs, and, of course, sharing purchase details.

Other platforms, such as the Little Redbook, combine group chat with the ability to share purchases across user networks.

Weibo (Twitter in China) also has an impact on influencers, such as “Mr. Bags” who set up hundreds of thousands of people around them. Weibo brand influence posts are now used for direct product promotion and sales, especially microblogging acquired by Alibaba.

It serves as a conduit for traffic storage, storing pages that are optimized for mobile devices and formatted for Chinese social networks.

The result of this more social-oriented approach is that brands now offer real-time customer service to their customers via WeChat, and even place QR codes on websites to guide users to their official web pages and instant messaging services. IM services also need to be provided on the site, but WeChat is the most trusted platform.

Mobile dominates the desktop

China’s entire digital landscape is the dominant mobile. By the end of 2015, China Mobile reached 2 trillion yuan (about 289 billion U.S. dollars) in business, an increase of 2000% over the previous year.

2016 projections show that mobile commerce accounts for about two-thirds of desktop sales, but looking at.

On the day of 2016 Singles Day, 82% of sales were on mobile devices, which could mean faster than expected. Undeniably, the trend is that mobile commerce will continue to grow both inside and outside China and eventually become the main way consumers buy online. Optimized store pages for mobile devices are more important than ever.

The shopping experience is more important than pricing According to a recent Kantar Retail Study, the primary motivation for Chinese consumers to shop online has shifted from “price, variety, and convenience” to “quality, value, service, and experience.

Chinese consumers are seeking richer “top-tier” experiences that will surely flow out of China. This reinforces the important factor in developing the importance of high-quality consumer shopping funnels in China. On average, the time to retain an online customer is 6-8 seconds.

This page must focus on Chinese consumers, with a focus on product presentation, choice, page design, navigation, and call-to-action. With the Chinese market evolving, how will this affect international brands? The situation is quite different from last year.

Cygnet intense competition Lynx unprecedented competition, Lynx and Lynx global competition increasingly fierce and saturated.

Big players can dominate here, but if your brand’s popularity or popularity in China is not high, it’s certainly not a “magic bullet.” So far this year, 15% of international brands have left the platform.